Senior US Treasury Official, Iraqi Prime Minister Hold Successful Meeting at UNGA

One big US concern was Iran's exploitation of Iraqi banks to evade sanctions, but that problem appears to have been resolved

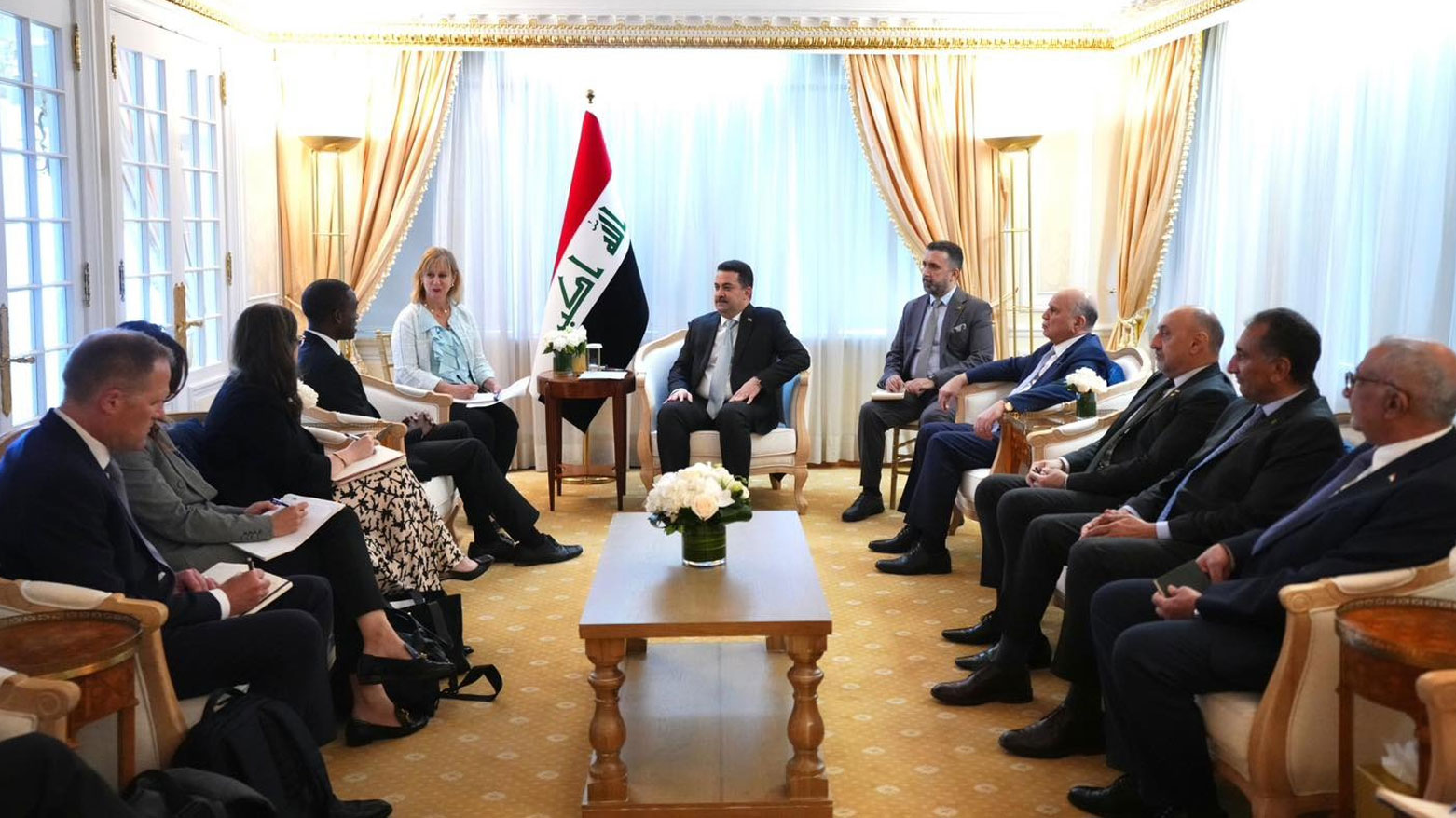

WASHINGTON DC, United States (Kurdistan 24) – Deputy Secretary of the U.S. Treasury Department Wally Adeyemo and Iraqi Prime Minister Mohammed Shi’a al-Sudani met on Monday on the sidelines of the opening of the UN General Assembly (UNGA.)

This marked Sudani’s second meeting that day with a senior U.S. official, as he also saw Secretary of State Antony Blinken.

Read More: Blinken ‘Emphasized Need to Reopen Iraq-Turkey Oil Pipeline’ in Meeting with Sudani

One of the biggest concerns Washington had regarding Iraq’s financial sector was that it was being exploited by Tehran to evade sanctions.

That problem appears to have been resolved, and the U.S. read-out of their meeting was broadly positive, including Adeyemo’s praise for the significant growth in Iraq’s non-oil economy

Iranian Sanctions Evasions through Iraqi Banks

The problem of Iran’s use of Iraqi banks to evade sanctions was rooted in a mistake made by the George W. Bush administration, when, in March 2003, it launched Operation Iraqi Freedom (OIF) to overthrow Saddam Hussein’s regime.

There were good, solid reasons for that war, rooted in traditional, national security concerns. But when OIF was launched, the Bush administration believed that it had already won in Afghanistan and that OIF would be equally easy.

Neither was true, of course. As a senior Pentagon aide later told this reporter, “We should have argued that overthrowing Saddam was necessary—not that it would be easy.”

That overconfidence bred a lack of rigor in the entire operation. It included how the new Iraqi government would obtain hard currency. The Bush administration looked to that government to be a big success—a model of democracy for the entire region.

So it provided Iraqi banks easy access to U.S. dollars, through the Federal Reserve Bank of New York. However, that mechanism was subsequently exploited by Iran to evade sanctions. The Wall Street Journal published a major report on this issue earlier this month.

The “New York Fed’s process to move Baghdad’s oil earnings lacked key money-laundering safeguards,” it said, “resulting in illicit transfers that financed terrorist groups for years.”

After Saddam’s overthrow, “Washington agreed to hold Iraq’s earnings from oil sales—tens of billions a year—at the New York Fed,” the Journal explained.

“To circulate the proceeds back into Iraq, the Fed began shipping dollars in cash to Baghdad and processing commercial wire transfers from Iraq’s private banks for international trade, hoping to revive its shattered economy after years of war and sanctions,” the Journal continued.

But the system “lacked a key check that is standard in international banking: it didn’t require the banks to divulge specifically who was getting the funds they were wiring out of Iraq.”

And that is how the U.S. ended up funding Tehran’s activities.

As early as 2012—over 10 years ago—the Obama administration was warned of the problem. But Barack Obama had opposed OIF. He thought it was an unnecessary war, driven by a hot-headed Republican president. To prevent a future such disaster, at least in Obama’s eyes, regarding Iran, as president, Obama fixed on establishing much better ties with Tehran.

That was behind his push for the Iranian nuclear deal. It also meant that he did not want to address the issue of Iran’s exploitation of Iraq’s banking system. Indeed, it was not really until the Biden administration that the U.S. took effective measures to deal with it.

The Federal Reserve has set up a pilot system in which dollar transfers to Iraqi banks go through a major U.S. bank, Citigroup, which does the standard due diligence that should have been done all along.

Thus, as the U.S. readout of the meeting between Adeyemo and Sudani states, they discussed “Iraqi banking sector reform, financial relations with the United States, and combatting illicit finance.”

Moving Away from Saddam Hussein’s State-Dominated Banking System

Under Saddam’s Baathist regime, many aspects of the economy were highly centralized, falling under the government’s control. That includes the banking sector.

Both the International Monetary Fund (IMF), as well as the U.S., have pushed for an end to that centralized system.

“The restructuring of banks is in line with the [Iraqi] government’s program for comprehensive banking reform,” Mudher Muhammad Saleh, Sudani’s Advisor for Financial Affairs, recently told Shafaq News.

“State-owned banks dominate 88% of banking sector investments, leaving only 12% for the private sector,” he said. “This imbalance has hindered competition and prevented the banking sector from reaching its full potential.”

Indeed, according to Mahmoud Dagher, a former official of Iraq’s Central Bank, two of the largest state-owned banks—the Rafidain and Rashid banks—remain under restrictions, dating back to Saddam’s 1990 invasion of Kuwait, which limit “their ability to conduct international financial transactions,” as Shafaq News reported.

But Sudani’s government has been working on addressing all these problems. Thus, “Deputy Secretary Adeyemo congratulated Prime Minister Sudani on Iraq’s significant progress on banking sector reform, which has broadened Iraq’s international financial connectivity and increased financial inclusion,” the U.S. readout said.

“Deputy Secretary Adeyemo emphasized Treasury’s support for the Central Bank of Iraq (CBI) and the Prime Minister’s reform agenda,” it continued, while he “also applauded Iraq’s 6.0 percent growth in the non-oil economy.”